[ad_1]

More young Americans are late to paying their car loans – approaching levels not seen since the Great Recession, according to a report from the New York Fed.

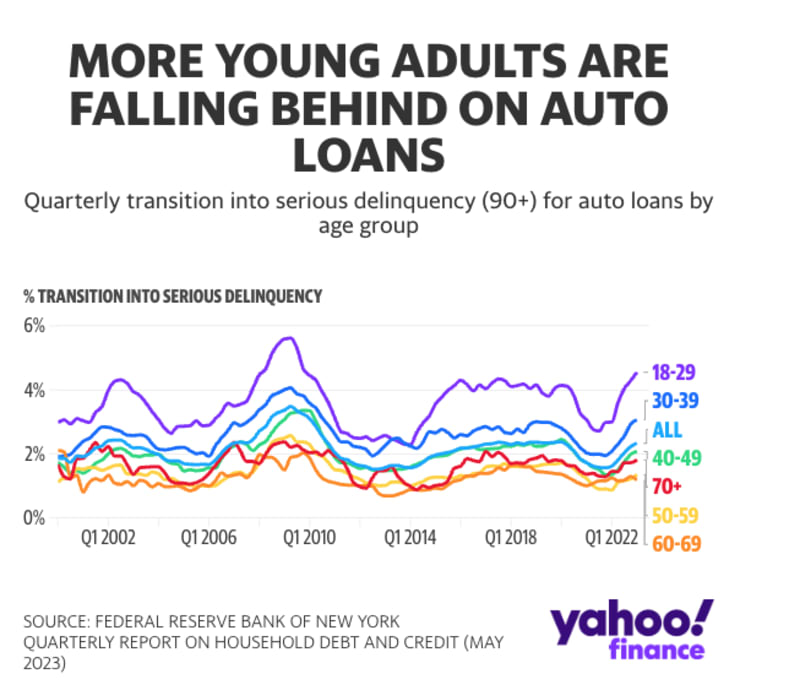

In the last quarter, 4.6% of borrowers under 30 transitioned into serious delinquency – meaning they were at least 90 days overdue on an auto loan payment. This figure is up from a year ago and is the highest percentage since the tail end of the Great Recession in 2009, when it was 4.7%.

Across all ages, the number of new auto loans and leases totaled $162 billion last quarter, down from last year, but an increase from the volume before the pandemic. Of all borrowers, 2.3% were at least 90 days overdue on making their auto loan payment.

The highest rate of serious delinquency was observed among younger Americans. Torsten Slok, the chief economist at Apollo Global Management, told Yahoo Finance that this age group was struggling because they are “more vulnerable” to the ongoing macroeconomic trends. (Apollo is the owner of Yahoo.)

For example, Slok said, the Fed’s hike of interest rates is presenting a challenge. Because younger Americans have comparatively little savings, they are less prepared to afford the additional costs incurred by the higher rates. Americans are paying around $50 to $60 more on new car loans this year because of the higher interest rates alone, according to Ivan Drury, the senior manager of insights at Edmunds.

Drury said that the financial outlook for car financing will only worsen if the Fed hikes interest rates again at its June 14 meeting.

The Fed has been increasing interest rates in an effort by the Fed to cool down inflation. That’s contributed to new car prices sitting at record highs at the end of last year. Bankrate.com’s chief financial analyst Greg McBride said that Americans do not have the cash on hand to afford those rising car costs up front, so their average loan payment is getting higher – and less affordable.

In other words, young Americans may be biting off more than they can chew when it comes to auto loans, making it harder to keep up.

“The payments are absolute budget busters,” McBride told Yahoo Finance. “The average car payment for new car buyers was $800 a month last year, [and] about one in seven buyers has a payment of at least $1,000 a month. There’s no wiggle room there.”

Beyond the payment increase, Drury explained that more car dealers are forcing customers to finance their car in 36 or 48 months. These shorter financing options are less affordable for those whose financial situations are more unpredictable, many of whom preferred longer payback periods.

Coming out of the pandemic, McBride said that delinquencies for car loans have increased “sooner” and “faster” compared to other loans, which he attributed to more lenient lending standards for borrowers with subprime credit scores. These lower scores are more common among younger Americans, according to Experian.

The rise in delinquencies for younger Americans comes as these borrowers face a likely reinstatement of student loan payments.

“That’s going to be very critical,” Slok said. “It’s a very significant amount of households.”

A third of Americans aged 25 to 34 have student loan debt.

“If the economy weakens and goes into a recession, we’re going to see a level of auto loan delinquencies that hasn’t been seen in a very long time, if ever,” McBride said.

Read the latest financial and business news from Yahoo Finance

Jared Mitovich is a writer at Yahoo Finance. Follow him on Twitter @jmitovich